Do you guys notify your home owner's insurance of every firearm and/or NFA item you have, including serial numbers and pictures where possible?

Mine is asking for this, but I told them I would document for my own records, and if needed, I would supply to them with a police report.

Thoughts? What about ammunition, do you give them a count of that? How do you assign a value to that?

Notify home owners insurance?

I took an extra policy on my firearms, because homeowners would only cover $2500.00 in the case of theft, fire, flood etc,and yes I had to give them model ,make, and serial number. For what it is worth I would check and see how much your homeowners policy will cover.I don't know about ammo.

"When they can't get their mind right,a well placed Donkey Punch or Mule Kick will do miracles."

-

Bendersquint

- Industry Professional

- Posts: 11357

- Joined: Sat Jan 07, 2006 7:19 pm

- Location: North Carolina

- Contact:

My policy required that I merely document what I have and send it to them and any changes in my "inventory" would require a notification letter.

No photos needed, or serials.

What I did to protect myself further was to photograph in detail my entire collection and save it as a PDF, I store it on a secure online server with a file date that is consistant with my inventory date. That way they could never say I inflated 'what I had' to enhance a claim. Its a bit far fetched but I would rather protect myself than be out the money if they say its BS.

Took about 8 hours to do it and about 20 minutes to update when neccesary. All the updates are kept online so there is a trail.

Works for me and I know its secure so there isn't a real worry for me.

-B

No photos needed, or serials.

What I did to protect myself further was to photograph in detail my entire collection and save it as a PDF, I store it on a secure online server with a file date that is consistant with my inventory date. That way they could never say I inflated 'what I had' to enhance a claim. Its a bit far fetched but I would rather protect myself than be out the money if they say its BS.

Took about 8 hours to do it and about 20 minutes to update when neccesary. All the updates are kept online so there is a trail.

Works for me and I know its secure so there isn't a real worry for me.

-B

-

Stu

- Silent But Deadly

- Posts: 4571

- Joined: Mon Mar 03, 2008 2:11 am

- Location: Wheat Ridge, CO

- Contact:

This is the way to go. Most home owners policies have a limit of $2,500 on guns and jewelry. Furs, cameras, cash, fine arts, and some other stuff is usually limited as well.Ga.Dawg wrote:I took an extra policy on my firearms, because homeowners would only cover $2500.00 in the case of theft, fire, flood etc,and yes I had to give them model ,make, and serial number. For what it is worth I would check and see how much your homeowners policy will cover.I don't know about ammo.

Here is another question. Do you treat serial numbers that are in a row as a pair and set? The insurance company probably won't, since it won't change the value of either firearm if you lose one.

-

ArevaloSOCOM

- Silencertalk Goon Squad

- Posts: 17511

- Joined: Sat May 20, 2006 1:22 am

- Location: London, England

- Contact:

-

Stu

- Silent But Deadly

- Posts: 4571

- Joined: Mon Mar 03, 2008 2:11 am

- Location: Wheat Ridge, CO

- Contact:

I doubt it. Well, maybe some people would. As soon as something becomes illegal, the policy no longer protects it. So if you see it coming, just cancel the policy because you 'sold' it all. Not like you need a reason to cancel.700PSS wrote:One thing to know: When, by the stroke of a pen, all our toys become "contraband", they will rat us out too.

Plus, what kind of asshole has so much time to spare while running their business to go through and rat out people with things like that insured?

I'll give you a hint to the answer:

How do you think illegals get insurance?

Oh, you know, the kind that get served with subpoenas.Stu wrote:Plus, what kind of asshole has so much time to spare while running their business to go through and rat out people with things like that insured?

"And by the way, if you're gonna take up a hobby of letter writing, you might want to learn how to spell "writing" you stupid F--k." - Nighthawk re kwikrnu

-

The Good Doctor

- Silent But Deadly

- Posts: 193

- Joined: Wed Apr 23, 2008 9:33 pm

- Location: Tupelo, Mississippi

- Contact:

Pretty much EVERY insurance company limits coverage on "theft of firearms" to $2,000 or $3,000 for FIREARMS AND RELATED EQUIPMENT. Therefore if you have over that much in firearms..... you won't be paid if someone steals them. The coverage is also ONLY for certain perils (things that can cause loss) like theft, fire, lightning, and a limited number of other causes of loss. So they are not covered for EVERYTHING That could happen. More on that later.

So to summ up your base policy: If you have a Preferred homeowner policies and have a fire you will probably be paid for all your guns for a "like kind" payment...the problem comes in when:

A. If there is a theft or something else happens that your home policy doesn't cover like flood, accidentally leaving your rifle in the woods over night....you will likely have limited coverage for theft or....NO coverage at all! That is NOT COOL.

B. If your gun has some "collector" or "rarity" value you could find yourself NOT paid the full value. That is also NOT COOL.

There are TWO ways to specifically insure your rifles to avoid these kinds of problems. First, generally you can schedule them on your home or tenants policy. Second, you can purchase separate coverage from some NRA program or something like that. I would suggest you insure them under your homeowners.

There are FOUR reasons why you would want to cover your guns separately:

---->1. Generally these endorsements have NO DEDUCTIBLE or a very low deductible.

---->2. You can insure the gun for its true VALUE, especially if there is some "collectible" or "rarity" aspect to it. For example, if someone steals my S&W low serial # shotty with the hand-carved relief image done by some great artist....I should schedule it. Your standard home policy will only pay you for a run-of-the-mill shotgun and not all those unique aspects. This may become more and more important as Obama bans guns and you can no longer buy another SBR PS90, SIG556, whatever...making some of the guns you have NOT REPLACEABLE.

---->3. The coverage is A LOT better inclduing coverage for crazy honest mistakes like "I left it in the woods by accident and when I returned it was gone" or "I was climing a rock and dropped it 300 feet down a cliff."

---->4. Listing them generally requires you to get your local gun broker to write a "formal" description and value.... establishing IN ADVANCE by an INDEPENDENT THIRD PARTY what exactly you have and what it is worth BEFORE something happens. This is ALWAYS a good idea and makes getting paid for your claim an absolute breeze. When something does happen you WILL feel awful.... but at least you can get your claim check fast and that WILL make you feel MUCH better. Trust me.

Of course there is a PREMIUM assocated with scheduling guns, so you decide if it is worth it. My own policy costs $11 per $1,000 of value. I currently have my two highest value rifles scheduled. The others I do not schedule, I will depend on the limited and not-as-broad coverage of my homeowners to cover these weapons.

Caution: Some company people are LIBERAL ANTI-GUN so don't be surprised if you have follow-up questions about "Why does the insured have a howitzer?" Personally I have yet to have an insurance company make a big deal out of anything my customers buy, but I have heard of someone having trouble at some point in the past.

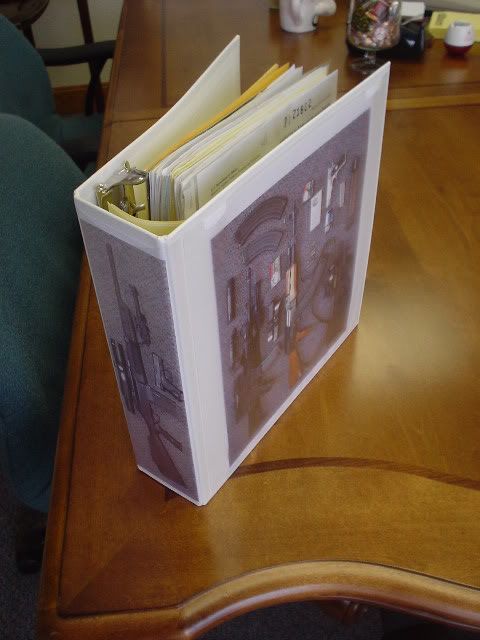

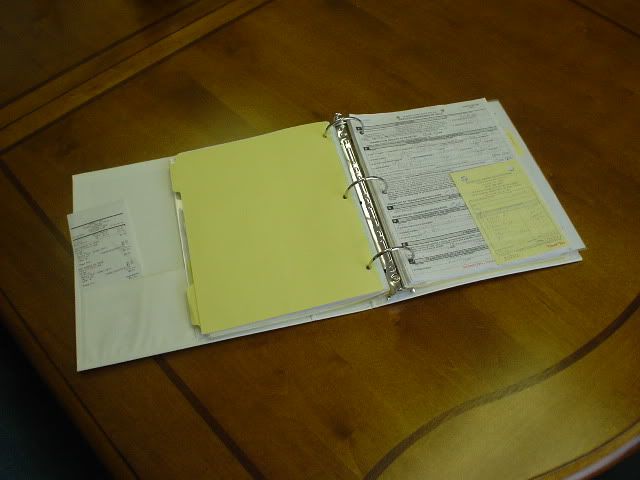

You SHOULD keep a book on all your firearms including photos, invoices, serial numbers, NFA tax stamps, etc. in a SEPARATE location. It is also a good idea to keep any firearms history in here for things like "added new trigger" or history like "This weapon used in so-and-so conflict by my grandfather William Schmortz" or whatever.

OK, so I am a little anal about documentation. Fortunately there are some huge long-term benefits of that kind of record keeping.

[Ick sits back and waits for the huge KUDOS rewards]

If you don't understand all this..... GO SEE YOUR INSURANCE AGENT and take the details of this post along with you.

So to summ up your base policy: If you have a Preferred homeowner policies and have a fire you will probably be paid for all your guns for a "like kind" payment...the problem comes in when:

A. If there is a theft or something else happens that your home policy doesn't cover like flood, accidentally leaving your rifle in the woods over night....you will likely have limited coverage for theft or....NO coverage at all! That is NOT COOL.

B. If your gun has some "collector" or "rarity" value you could find yourself NOT paid the full value. That is also NOT COOL.

There are TWO ways to specifically insure your rifles to avoid these kinds of problems. First, generally you can schedule them on your home or tenants policy. Second, you can purchase separate coverage from some NRA program or something like that. I would suggest you insure them under your homeowners.

There are FOUR reasons why you would want to cover your guns separately:

---->1. Generally these endorsements have NO DEDUCTIBLE or a very low deductible.

---->2. You can insure the gun for its true VALUE, especially if there is some "collectible" or "rarity" aspect to it. For example, if someone steals my S&W low serial # shotty with the hand-carved relief image done by some great artist....I should schedule it. Your standard home policy will only pay you for a run-of-the-mill shotgun and not all those unique aspects. This may become more and more important as Obama bans guns and you can no longer buy another SBR PS90, SIG556, whatever...making some of the guns you have NOT REPLACEABLE.

---->3. The coverage is A LOT better inclduing coverage for crazy honest mistakes like "I left it in the woods by accident and when I returned it was gone" or "I was climing a rock and dropped it 300 feet down a cliff."

---->4. Listing them generally requires you to get your local gun broker to write a "formal" description and value.... establishing IN ADVANCE by an INDEPENDENT THIRD PARTY what exactly you have and what it is worth BEFORE something happens. This is ALWAYS a good idea and makes getting paid for your claim an absolute breeze. When something does happen you WILL feel awful.... but at least you can get your claim check fast and that WILL make you feel MUCH better. Trust me.

Of course there is a PREMIUM assocated with scheduling guns, so you decide if it is worth it. My own policy costs $11 per $1,000 of value. I currently have my two highest value rifles scheduled. The others I do not schedule, I will depend on the limited and not-as-broad coverage of my homeowners to cover these weapons.

Caution: Some company people are LIBERAL ANTI-GUN so don't be surprised if you have follow-up questions about "Why does the insured have a howitzer?" Personally I have yet to have an insurance company make a big deal out of anything my customers buy, but I have heard of someone having trouble at some point in the past.

You SHOULD keep a book on all your firearms including photos, invoices, serial numbers, NFA tax stamps, etc. in a SEPARATE location. It is also a good idea to keep any firearms history in here for things like "added new trigger" or history like "This weapon used in so-and-so conflict by my grandfather William Schmortz" or whatever.

OK, so I am a little anal about documentation. Fortunately there are some huge long-term benefits of that kind of record keeping.

[Ick sits back and waits for the huge KUDOS rewards]

If you don't understand all this..... GO SEE YOUR INSURANCE AGENT and take the details of this post along with you.

-----

Ick

Ick